PLUS: Australia’s efforts in Green-Mining of Critical Minerals. The Collaborative Battery Race: Australia–Asia’s Push to Power a Renewable Future

As the global transition to clean energy accelerates, the race is on to develop scalable, affordable, and sustainable energy storage solutions. Batteries lie at the heart of this transformation—essential not only for stabilising renewables like wind and solar, but also for ensuring energy security across Australia’s vast landscape and the Asia-Pacific. In this dynamic race, Australia and its regional neighbours are fast becoming powerhouses of innovation and investment.

Australia: A Raw Materials Powerhouse with R&D Muscle

Australia’s abundant reserves of lithium, cobalt, and nickel—core components of lithium-ion batteries—have already positioned the country as a critical supplier in the global battery value chain. Companies like Mineral Resources Limited, Pilbara Minerals, and IGO Ltd. are expanding operations, while the federal government’s National Battery Strategy, announced in 2024, aims to build a competitive sovereign battery manufacturing sector by 2030.

The environmental impact of companies like Mineral Resources Limited, Pilbara Minerals, and IGO Ltd., which are major Australian suppliers in the global battery value chain, is complex and evolving. While these companies are essential to the clean energy transition—particularly as providers of lithium and other critical minerals used in batteries—they also face significant scrutiny over their environmental and social impacts.

Environmental Impact Overview

a. Land Disruption & Water Use

- Open-pit lithium mining, the dominant method in Australia, causes extensive land disruption.

- It also consumes large amounts of water, which is especially sensitive in arid regions like Western Australia.

- Mining activities can lead to habitat destruction and impact biodiversity if not well-managed.

b. Carbon Emissions

- Though lithium mining enables low-carbon technologies like EVs and renewable energy storage, the mining operations themselves are fossil-fuel intensive, especially in upstream extraction and processing.

c. Waste & Chemical Use

- Lithium processing generates waste products, including tailings that may contain harmful substances if not properly contained.

- Chemical leaching and storage risk contaminating groundwater if mishandled.

Are They “Green Certified”?

There is no single, universally accepted “Green Certification” for mining. However, companies may adhere to frameworks or initiatives that aim to improve ESG (Environmental, Social, and Governance) performance.

Here’s a snapshot of each:

✅ IGO Ltd.

- IGO has positioned itself as a leader in ESG transparency in the Australian mining sector.

- It publishes annual Sustainability Reports aligned with Global Reporting Initiative (GRI) and Task Force on Climate-Related Financial Disclosures (TCFD).

- IGO is a member of the International Council on Mining and Metals (ICMM), which requires high environmental and ethical standards.

- They’ve stated ambitions to power operations with renewable energy and reduce Scope 1 and 2 emissions.

⚠️ Pilbara Minerals

- Pilbara Minerals is working to improve ESG practices, and has made public commitments to decarbonisation and tailings management.

- It collaborates with partners to reduce emissions in the lithium hydroxide refining process.

- Not formally “green-certified,” but is increasingly subject to investor and stakeholder pressure to align with sustainable mining benchmarks.

⚠️ Mineral Resources Limited (MinRes)

- MinRes has faced criticism over environmental management, including fines for unauthorised land clearing and emissions breaches.

- However, it has taken steps to publish climate action plans, increase water recycling, and invest in electric mining fleets.

- The company is not currently considered a leader in sustainability but is making progress under investor scrutiny.

Industry Sustainability Efforts

Several industry-wide efforts aim to standardize and certify “green” mining, including:

- IRMA (Initiative for Responsible Mining Assurance)

- The Lithium Stewardship Initiative

- OECD Due Diligence Guidance for Responsible Mineral Supply Chains

- ESG performance ratings by third-party assessors like MSCI, S&P Global, or Sustainalytics

Summary

| Company | ESG Status | Green Certification | Notable Points |

| IGO Ltd. | Strong ESG performer | Member of ICMM | Strong disclosures, TCFD alignment |

| Pilbara Minerals | Improving ESG profile | No formal green cert. | Working on sustainable lithium refining |

| Mineral Resources Ltd. | Mixed record | No formal green cert. | Criticised in past, making gradual improvements |

Melbourne-based startup Recharge Industries, which acquired the collapsed UK battery startup Britishvolt, is building one of the world’s largest lithium-ion battery gigafactories in Geelong. Meanwhile, CSIRO is supporting next-generation battery R&D, including sodium-ion and solid-state technologies that could lower costs and reduce environmental impacts.

The recent Melbourne-based Victoria Cleantech Cluster showcased clean technology solutions and conference with sector exhibitors including Battery storage. Check exhibitors Here+

Japan and South Korea: Tech-Driven Scaling

Longtime leaders in battery technology, Panasonic (Japan) and LG Energy Solution (South Korea) continue to expand their manufacturing and R&D presence across Asia, including partnerships with Australian mining and technology firms. South Korea’s POSCO Future M has invested in lithium refining projects in Queensland, ensuring upstream control in the clean energy supply chain.

These countries are also investing heavily in recycling and circular economy solutions. Japan’s Toyota and South Korea’s SK Innovation are leading efforts to close the loop on battery waste, reducing dependence on virgin materials and extending battery life cycles.

China: Dominating the Global Supply Chain

China continues to dominate global battery manufacturing, producing more than 75% of the world’s lithium-ion batteries. Companies like CATL (Contemporary Amperex Technology Co. Ltd.) and BYD are expanding aggressively across Southeast Asia, building gigafactories in Thailand, Indonesia, and Vietnam to meet growing regional demand. CATL’s new sodium-ion batteries, launched in 2023, are being positioned as a game-changer for stationary storage and two-wheeled transport markets.

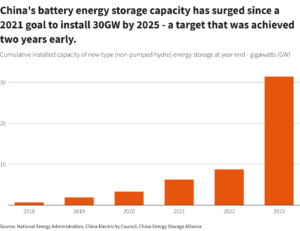

China is experiencing a boom in battery storage. This growth is driven by government policies, the need for grid stability and increased energy demand from renewable sources. Shandong’s new plant incorporates both lithium ion and vanadium redox flow batteries, according to a report by local state media. Vanadium is a newer technology that promises longer storage times and improved safety.

Graphics credit: Reuters

China’s Belt and Road Initiative also includes energy storage infrastructure, with joint ventures and technology transfer agreements accelerating deployment in partner nations.

Southeast Asia: Emerging Hubs and Partnerships

Southeast Asian nations are rapidly positioning themselves as manufacturing and logistics hubs in the global battery economy. Indonesia, with the world’s largest nickel reserves, has inked deals with Hyundai and LGES to establish EV battery factories. The government aims to be a key player in the global EV supply chain by 2027.

Singapore and Malaysia are investing in advanced battery R&D and piloting microgrid storage systems to ensure grid stability. Meanwhile, the Philippines and Vietnam are exploring public-private partnerships to scale renewable storage and integrate community-level battery projects.

Investing in the Future

Cross-border collaboration is key to scaling battery storage in a way that is commercially viable and environmentally responsible. Asia-Pacific Battery Alliance—a proposed multilateral platform—aims to facilitate coordination between governments, investors, and startups to accelerate innovation, harmonise standards, and de-risk supply chains.

Investors are taking note. Global clean tech VC investment in Asia-Pacific battery technologies reached US$5.3 billion in 2024, with Australian and Singaporean funds increasingly backing early-stage ventures focused on battery software, analytics, and recycling.

Conclusion: Collaboration Is Power

No single country can win the battery race alone. The path to decarbonisation demands deeper collaboration across research, finance, policy, and production. Australia–Asia’s diverse strengths—from raw materials and manufacturing to innovation and market demand—make it a uniquely positioned bloc to lead the charge in renewable energy storage.

As energy needs grow and climate targets loom, the real winners will be those who work together—building not only better batteries, but also a more resilient, sustainable, and interconnected energy future.